Primrose and Penny Meet Again Many Years Later at the Old Mansion That Has Now Become What

[Hey y'all! I found out that one of my favorite podcasters has been tracking ALL of his expenses for over half dozen years now, and asked him if he'd requite us an inside await at them. You know, cuz we're nerds like that ;) Patently he'south never looked at the overall picture before, and so we're the first people to see what'southward hiding in the numbers! Enjoy!]

In January 2010, I was wrapping up my last few classes of my MBA at Pepperdine University in beautiful Malibu, CA. One of my first assignments in the new year's day was simple:

Track all of my income and expenses for one week and write about the experience.

The merely rule: to track every single penny in and out of my life, whether it was spending thousands on a motorcar or finding a quarter on the street.

This was right up my aisle – as a data-obsessed Excel nerd and Myers-Briggs blazon ISTP, besides known as "The Craftsman," I quickly built a spreadsheet to help me track it all, complete with pin tables to summarize the information by date and category (read through to the end to get the Excel template).

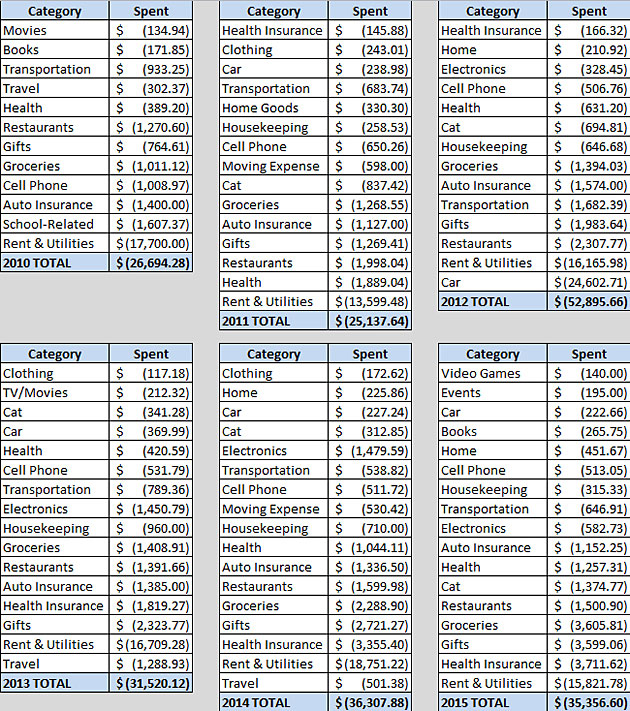

Over six and a half years and 7,500 rows after, my spreadsheet is alive and well, withal summing up my income and expenses into pretty charts.

While I watch my overall financial health every calendar month and twelvemonth and intermission it apart by category during tax season, I've never saturday down and looked at the key takeaways — that is, until J. Money asked me to.

Today, I'm going to exercise something I've never done: I'grand going make my expenses public and share seven surprises of this experiment:

Surprise #1 — Living with Roommates Didn't Salve Me a Ton

In the last 6 years, I've lived in 6 different places in Southern California and in 4 different roommate scenarios. I went from a "Seinfeld" phase (living alone in a i bedroom flat in Santa Monica, CA) to a "New Girl" or "Golden Girls" stage when I had iii roommates at a firm in West Hollywood, CA, and everything in between.

Yep, the rent & utilities were significantly cheaper in the latter ($13,500 vs. $17,700 living lone), but living with roommates brings in additional expenses:

- Cleaning was difficult, and then we got a housekeeper (-$650/yr)

- My groceries went upwardly because non everything gets split up perfectly and food & supplies might "go missing" (-$250/year)

- Eatery expenses increased because I was around more friends and acquaintances and was pressured to get out with them (-$750/year)

- I spent a lot more on "gifts" (-$500/year)

Adding those factors in, I was still saving $two,000/twelvemonth on hire, merely that only equates to $166/month, which I probably could've negotiated when I lived alone, or constitute a comparable apartment for that much less. Too, I wasn't sharing a kitchen, family room space, and parking—instead, when I was living alone, I used every square inch of my flat and lived on my own terms.

If you lot're deciding to live with roommates, these are things to consider. Is it worth information technology to salve $100-200 on hire to bargain with the complexities of having one or more roommates? For many people, similar me, that extra toll makes sense… or peradventure you're an extrovert and only beloved having people around.

Surprise #2 — Having a Significant Other Has Been Expensive For Me

How does your human relationship status affect your finances? Here'south how it affected mine.

When I was single, I spent somewhere around $1,000/twelvemonth on gifts, but in one case I was in a relationship this more than than tripled! It didn't mean I was spending a lot more on my girlfriend, necessarily, just when you're a couple, you get invited to all sorts of appointment parties, weddings, birthdays, infant showers, and more, and you'll likely be chipping in for the gifts equally well. Add in gifts for your significant other and his or her family, and it'southward piece of cake to meet that y'all'll be spending much more than normal.

But that's not all. While your groceries and restaurant expenses could stay the same if everything is split up evenly, you lot'll likely attend more events equally a couple, so information technology'southward safe to presume that expenses will go upwardly in multiple ways.

For me, the gifts category was the most noticeable: I spent a whopping $3,600 in gifts in 2015 compared to $765 in 2010. While a good portion of the gifts went to family, I dove in to the line level and found that this was indeed mostly due to the change in relationship status.

Surprise #3 — Cat Ownership Isn't as Expensive as I Thought

This clearly depends on your parenting preferences, but luckily, I've done it both ways:

In 2014, I was very relaxed with my true cat—mayhap ane vet date, she was fed dry kibble, and she didn't demand a litter box because she went outside. She was also old enough that she didn't need toys and distractions. Cat-related expenses were very minimal.

True cat bills in 2014: $312

Compare that with the very adjacent year, when I took a more proactive approach: I fed her loftier-quality, raw cat food and had a couple of her broken teeth extracted by the vet'southward recommendation.

Cat bills in 2015: $1,375

That'south a $1,000 difference, only even in the more than expensive case, $115/calendar month, or less than $4 a day, to give my cat the best and take a furry friend around was worth it for me.

Surprise #iv — "Gold" or "Platinum" Health Insurance Hasn't Been Worth It

Being cocky-employed is expensive. It feels much worse than receiving a paycheck from a visitor considering I have to pay quarterly taxes on my income, which is about a third of my earnings. On elevation of that, I have to pay for my own health insurance.

As a hypochondriac, I opted for the "Gilded" plan, thinking that information technology would be better long-term. Merely just three years after quitting my steady job, I'm worth $viii,800 less due to monthly wellness insurance costs, and to add insult to injury, I've simply used my "awesome" gold plan a couple of times.

Average toll per yr: $3,500, or roughly 10% of my total expenses

Surprise #v — Tax Season is Non Only a Cakewalk, Simply Likewise Fun!

I don't remember yous'll hear this anywhere else… Ignoring quarterly taxes, I enjoy tax season. This is what it consists of:

- Sort my spreadsheet by date and category

- Eliminate the categories that aren't applicable

- Send it to my auditor

Done. This whole process takes a few minutes and information technology's fun to run across the yr equally a whole.

Surprise #vi — Despite the Odds of Winning, Playing the Lottery Makes Sense (to Me)

Everyone has their stance on this, and mine is somewhere in the middle. I only play the lottery if the expected return is greater than the cost of the ticket.

Basic math shows that your odds of winning the lottery, or at least matching all the numbers, are horrific. Only basic math too shows that when the lottery reaches certain thresholds, your expected return is really really good when you accept into account the smaller prizes. On top of that, the law of utility makes a great example: even if you played $1 on the lottery twice a week, you'd only be spending around $100/yr.

Is that going to ruin your finances? Probably not if y'all're reading this article. However, if you won, would it touch on your life? Near definitely… and that's why I play. The lottery also gives back to schools which I like.

Equally for the numbers, I've spent less than $400 in 6 years on the lottery and won back 10%. Is $1 a calendar week worth a take chances to win $100,000,000 or even $i,000,000,000? For me information technology is.

Surprise #7 — The Juicy Details Aren't Actually That Juicy

The numbers are fun and tracking finances to this level of item makes tax flavor enjoyable, but to me, the biggest bear on of this experiment has been my attitude.

Only one calendar week of tracking every penny in and out of my life was enlightening, but peradventure not in the way you'd look. I thought I'd discover insights almost the bodily information and where I could save money, and while that was somewhat true, the bigger lesson was one of sensation.

Every time I spent whatever amount of money, I was thinking about my new spreadsheet: the fact I'd have to spend time updating my table for this trivial buy, what it would mean to my rest, and if this expense was actually "worth it." This unproblematic homework assignment threw me out of "automobile-consumption" mode and made me question every purchase I made. It's like a meditative practice for minimalists.

After 6 years of doing this, that awareness is stronger than ever. I know what I tin can afford. I know what it'll mean if I make a large buy or if I take on a new monthly expense. It'southward easy to run across how this volition impact my bottom line and my future finances.

My Challenge For Y'all (And The Downloadable Template!)

This jolt of mindfulness and awareness is the reason I ask listeners of my podcast to go through this challenge. Track every penny in and out of your life – just for a week. Try it. There's no harm.

If you struggle and fail, no worries; merely if you succeed and you tin proceed doing it for a calendar month, a year, or more, your awareness will continue to ameliorate and y'all'll know exactly what you spend & make and more than importantly, what you can afford to spend or make.

Does it make sense to move? Tin can I afford to quit my job to commencement a business?

These questions are easy to answer when all the numbers are nicely summed up past category. Best of all, it only takes a couple of minutes a 24-hour interval to log your receipts if you lot stick with it.

While I only give abroad my spreadsheet template to listeners of my podcast, I've made it available to Budgets Are Sexy readers today. Grab the spreadsheet here, complete with macros (Excel automation) that I hand-coded myself, and watch the video tutorial here.

Snapshot of All My Numbers

Let's face up it… this is probably why you're notwithstanding reading this article. Y'all want to see my actual numbers and compare information technology to your own numbers, whether they're in your head, on Mint (or YNAB or EveryDollar), or in a spreadsheet.

Well, alright, but all I ask is that you don't judge me. I'm open to advice and effective criticism, merely let'due south keep this positive. I'm not putting all this financial information up only to be torn down. :)

Feel free to look over my numbers and share your ideas for improvement, your own feel tracking your income & expenses, and whatever other relevant commentary. I'll be here, stalking the comments.

Past the way, I've taken out yearly expenses that were less than $100 (like the lottery expense or my incredibly cheap haircuts) and more rarely, stuff that I didn't think would add value to this chat (similar accountant fees, commuter's license renewal, etc.), just to continue this as clean and relevant as possible.

At present that that'due south out of the way, bask this window into my personal life!

*******

Justin Malik is a serial entrepreneur who launched a podcast every bit a social experiment to help come to terms with performance-based social anxiety. In his podcast, Optimal Living Daily, he reads to y'all from the best blogs he can find, covering personal finance, personal evolution, minimalism, and more (with author permission of form). Bloggers read on his show, and his spin-off podcast, Optimal Finance Daily, include J. Coin himself of BudgetsAreSexy.com, IWillTeachYouToBeRich.com, MrMoneyMustache.com, TheMinimalists.com, Sivers.org, MarcAndAngel.com, and many more than. Learn more at OLDPodcast.com.

Jay loves talking about coin, collecting coins, blasting hip-hop, and hanging out with his three cute boys. You can check out all of his online projects at jmoney.biz. Thanks for reading the blog!

washingtontheridly.blogspot.com

Source: https://www.budgetsaresexy.com/learned-tracking-every-last-penny/

0 Response to "Primrose and Penny Meet Again Many Years Later at the Old Mansion That Has Now Become What"

Post a Comment